Introduction:

Firms devise several strategies to maximise their profits, sometimes, however, the market conditions turn out to be favourable such that even without any wise investment decisions or innovative improvements in production capacities, they accrue extraordinarily; non-historical profits. These out-of-the-blue profits are termed Windfall gains/profits. These gains may occur due to fortunate extrinsic factors like supply chain disruptions, natural calamities, wars, or a price spike. Being unexpected and unforeseen, these surplus funds received by the industry/ firm may be used for business expansion and further investment, increased dividends, a special one-time dividend, debt reduction, or a share buy-back.

Due to frequent price fluctuations, windfall profits can typically be accrued in the oil and gas sector. Several energy companies have incurred these gains throughout history, arising from sudden price spikes due to supply shortages. These profits can be both short-lived as well as long-term gains.

Various governments across the globe tax the companies that earn profits from windfall gains. These taxes are charged by the governments based on certain situational credentials. The recent slapping of a tax of Rs. 23,250 per tonne on domestically produced crude oil by the Indian government has added yet another entry to the list of countries that charge windfall taxes.

Windfall tax in India:

Having reduced the excise duty on petrol and diesel recently to check the soaring inflation, the government now has imposed a windfall tax on domestic producers like Oil and Natural Gas Corporation (ONGC), Oil India Limited, Vedanta Ltd, Reliance Industries (RIL), etc. This windfall tax is expected to earn the government revenues that would cover at least up to USD 12 billion (94,800 crores) in the remaining fiscal year. The government can, thereby, recover nearly 85% of its revenue loss incurred due to excise duty cuts.

This tax has been introduced to regulate the domestic oil producers who produce crude oil and sell it at international parity prices. This crude oil is produced domestically and is sold to domestic refineries only, but at prices prevailing internationally. Therefore, if prices spike due to some extrinsic factors like the ongoing Russia-Ukraine conflict, international prices shoot up. Since the domestic producers sell at international parity prices, their selling price also shoots up and so does revenue, since the manufacturing cost remains constant.

This has earned companies massive profits without any progressive efficiency updates and inputs from the company, thereby categorised as windfall gains. These supernormal, bumper profits accrued by the oil and gas firms triggered the imposition of this tax.

ONGC reported a net profit of Rs. 40,306 crores on total revenue of Rs. 1,10,345 crores in FY 2021-2022. This amounts to a massive net profit of 36.527% as a percentage of total revenue. On a similar footing, OIL recorded a net profit of Rs. 3887.31 crores in the fiscal. Vedanta’s Cairn Oil and Gas also recorded extraordinary profits. These profits especially soared in the March quarter, when the international prices of crude oil hit a record 14-year high of $139 per barrel.

The tax would charge the companies Rs. 23,250 per tonne. Given the conversion of a tonne to a barrel of crude oil as:

1 Tonne= 7.49 barrels,

The tax nearly amounts to Rs. 3,104.138 per barrel. Given the fact that:

1 Barrel= 158.987 litres

The tax amounts to Rs. 19.524 per litre of crude oil produced domestically.

The Calculation of domestically produced natural gas prices in India:

As per the New domestic Natural Gas Pricing Guidelines, 2014 issued by Ministry of Petroleum and Natural Gas, determination of domestic natural gas prices on a half-yearly basis is done by using the following formula:

Where,

- VHH is theTotal annual volume of natural gas consumption in USA and Mexico;

- VAC is theTotal annual volume of natural gas consumption in Canada;

- VNBP is theTotal annual volume of natural gas consumption in the European Union;

- VR is theTotal annual volume of natural gas consumption in Russia;

- PHH is the annual average of daily prices at henry hub, less US$0.50/MMBTU in consideration of transportation and treatment charges;

- PNBP is the annual average of daily prices at Natural Balancing Point, less US$0.50/MMBTU in consideration of transportation and treatment charges;

- PAC is the annual average of monthly prices at Alberta hub, less US$0.50/MMBTU in consideration of transportation and treatment charges;

- PR is the annual average of monthly prices as published by the Federal Tariff of the Russian Government.

Under the Ministry of Petroleum and Natural gas, The Petroleum Planning and Analysis cell publishes the half-yearly prices of natural gas using the formula prescribed above. This is also accompanied by a price ceiling, given the nature of the commodity and its enormous impact on inflation in any economy. Nature of the pricing, over the years, since the prescription of the formula as discussed has been as depicted by the chart below:

MMBTU: It is an acronym for Metric Million British Thermal Unit, which is a unit used to measure heat content or value of energy. Technically defined as the amount of heat required to raise the temperature of one pound of water by one Fahrenheit.

GCV: It is an acronym for Gross Calorific Value, defined as the amount of heat released by the complete combustion of a given mixture.

The price at which crude oil produced domestically is sold to the domestic refineries in the international parity price. This brings about a correspondence between the profits of ONGC and these prices. The profits earned by ONGC are as depicted by the chart:

Profit before Interest, Depreciation & Tax: Also known as EBITDA (Earnings before Interest, Depreciation, Taxes and Amortisation), it is used as a measure of the overall performance of a firm and also as the net income.

The following curve shows the price of Natural gas internationally as per the Henry Hub standards ($/MMBTU):

Relationship and similarity can be easily noticed between the three curves.

Analysis of the Tax Imposition:

Considering the enormous windfall gains made by the oil producers as well as the profits they incur in exporting petrol and diesel while petrol pumps in certain states are running dry, the government has imposed a windfall tax as discussed plus an export duty of Rs. 6 per litre on petrol and Jet Fuel (ATF : Aviation Turbine Fuel) and Rs. 13 per litre on export of diesel, with implementation from 1st July, 2022. The government in May cut the excise duty on petrol by Rs. 8/litre and on diesel by Rs. 6/litre.

The excise duty cut is expected to cost the government a massive amount of Rs. 1 Lakh crore. However, given the new tax on crude oil producers like ONGC, OIL and Vedanta, the government is expected to accrue more than Rs. 69,000 crores annually, given the fact that production in the 2021-22 fiscal year was 29.7 million tonnes. This amount for the rest of the current fiscal year is estimated to be Rs. 52,000 crores. In addition to the amount obtained from windfall taxes, the export duty is also expected to earn revenue. During the months of April and May, India exported 2.5 million tonnes of petrol, 5.7 million tonnes of diesel, and 797, 000 tonnes of ATF. This export tax, if continued until March 2023, is expected to earn a massive revenue of Rs. 20,000 crores, even if the export value falls down by 70%.

The combined revenue from both the taxes is expected to cover-up nearly 85% of the revenue loss that the government incurred due to excise duty cuts. ‘Phenomenal Profits’ have been earned by the concerned players from the purchase of discounted Russian Oil and the export to regions such as Europe that are avoiding Russian oil. Meanwhile, several petrol pumps in certain states of the nation like Madhya Pradesh and Rajasthan ran dry, because the producers preferred to export the oil rather than cater to the domestic needs. The government, hence has clearly adopted a twin-pronged approach, firstly by disabusing exports to cater to domestic needs, and secondly by taxing the supernormal profits made by the firms to finance its developmental projects.

Another rule devised by the government requires the firms to sell petrol in the domestic market at an amount equal to half of what they export for the current FY. For diesel, the percentage decided upon is 30% of exports. With exports being discouraged and a simultaneous increase in custom duties for gold will widen the current account deficit.

Future of the Tax:

The government will review the windfall tax on crude oil every two weeks based on exchange rates, international crude oil prices and its local cost.

Implications for Firms:

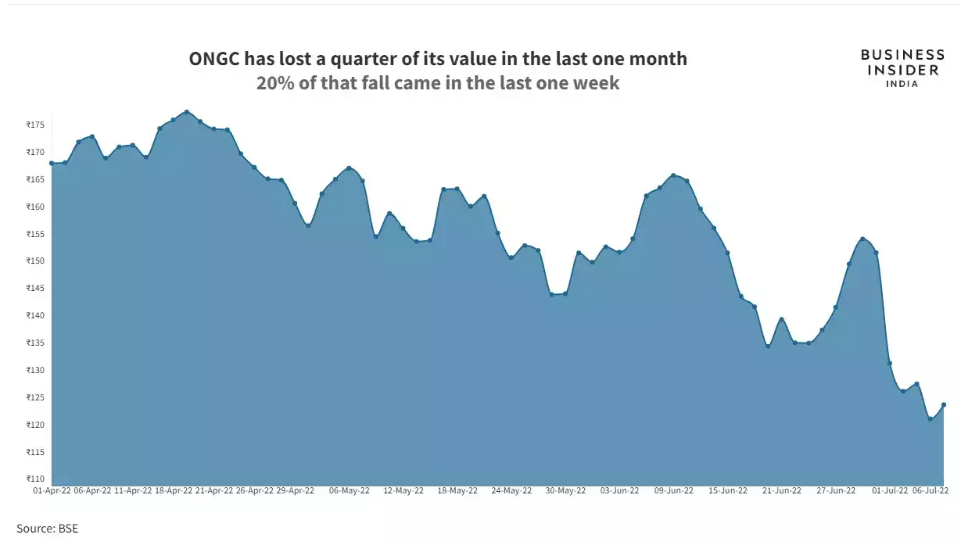

The surplus funds received by the industry/ firm may be used for business expansion and further investment, increased dividends, a special one-time dividend, debt reduction, or a share buy-back. Therefore, the imposition of windfall tax on the profit is a direct hit to the dividend that the investors shall receive out of the investment in a particular firm. ONGC has clearly been adversely affected by the taxes and evidently has lost more than USD 5 billion in market value since its earnings and profits are now checked by the taxes. This has resulted in the company losing a fifth of its value in seven days only. Imposition of the tax clearly took a toll on the values of the shares of several companies in the industry.

Share price chart of ONGC highlights the severity of the implication:

It is also speculated that due to the said reasons and the taxes, ONGC might experience a decline of earnings by 14% for the full Financial Year 2023-24. The speculation for target price cut is 16%. These have been predicted by analysts at HDFC Securities. JM Financial Analysts also cut profit estimates for ONGC by 8% for FY2023 and by 4% for FY2024.

|

Brokerage |

Recommendation |

Target Price |

Upside/Downside |

|

HDFC SECURITIES |

BUY |

184 |

50% |

|

EMKAY GLOBAL |

BUY |

185 |

50% |

|

SHAREKHAN |

HOLD |

140 |

14% |

The situation for ONGC and others are further threatened by the fact that oil prices globally have started to come down slowly, which increases the prospects of lower profits. However, considering the lowering oil prices, there are speculations that the government may revise taxes. If revised, the implementation would be immediate, as a result of which the companies are expected to gain in the stock market.

Countries Apart from India that levy Windfall Tax:

- Australia:

The Island nation of Australia levies windfall tax as the Commonwealth places windfall tax and franchise fees windfall tax.

Commonwealth Places windfall tax is designed to protect state revenues from claims for refunds in relation to certain taxes applied in commonwealth places. - Mongolia:

Mongolian government holds the record for the highest tax windfall tax in the world on unsmelted copper and gold concentrate produced in the nation. This tax was imposed on mining companies in 2006 and was repealed in 2009 to attract foreign investment in the sector. - United Kingdom:

The first one-off (only for once) Windfall tax was introduced by the government in 1981 on certain bank deposits. This was followed by a tax on privatised utility companies in 1997, and recently, the government has imposed a tax on energy companies. - United States of America:

‘Crude Oil Windfall Profit Tax’ was introduced in 1980, and the aim of the tax was to acquire the massive profits earned by producers due to the OPEC embargo that led to a massive price hike. - Scandinavia:

The region includes Denmark, Norway, Sweden and a few other nations. Sweden in 2008 imposed taxes on sectors earning windfall profits, such as hydro-power and nuclear power. Norway also imposed a tax on hydroelectric power plants in 2009 and Finland announced a tax on nuclear as well as hydro power plants in 2010.

Further discussions: Why Only the Oil and Gas Sector?

Over a period of time, several countries have taxed their oil and gas sectors as the profit from war-fuelled prices. This profiteering has been cut short recently by India also as discussed above. These Windfall gains earned by the producers of oil and gas cause the prices to rise for the end consumer, and since the products of this sector are value additions or input to all other sectors producing consumer goods, a spike in the price of oil and gas causes price levels to rise. This makes the situation of the end consumer vulnerable and miserable. However, by taxing these firms, the government utilises surplus funds gained to finance welfare and relief programs, which reduces to some extent the impact of price rise on the end consumer.

Does Big Tech also deserve a Windfall Tax?

During the world-wide lockdowns triggered by COVID-19, social and economic dependence on technology increased massively. This led to massive profits for tech giants, and is evidently a windfall gain as the demand spurge is something which no firm is responsible for. Since people now had to rely on devices to earn, learn, shop and connect, the sales of tech giants sky-rocketed, something that can be clearly interpreted by the net profit soar of 80% for Amazon in 2020. Since the big players made huge profits and those were not taxed, the competition in the market has also been significantly reduced.

Evidently, the lobbying by big-tech firms has been extraordinarily successful, and on the top of that, the situation turned out to be favourable. With people dying, factories shut, economies collapsing because of the pandemic (Sri Lanka- Clearly the best example) the governments and people had better things to take care of and check, than the profit of mighty technology giants.

References:

- https://en.wikipedia.org/wiki/Krishna_Godavari_Basin

- https://www.statista.com/statistics/262860/uk-brent-crude-oil-price-changes-since-1976/

- https://www.ppac.gov.in/WriteReadData/CMS/201501270457045609772DatasourcesforpricecalculationNov14-March-15.PDF

- https://www.henergy.com/conversion

- https://www.adanigas.com/png-commercial/explore-mmbtu

- https://en.wikipedia.org/wiki/Billion_cubic_metres_of_natural_gas

- https://www.macrotrends.net/2478/natural-gas-prices-historical-chart

- https://www.macrotrends.net/1369/crude-oil-price-history-chart

- https://www.ppac.gov.in/content/7_1_ForecastandAnalysis.aspx

- https://economictimes.indiatimes.com/news/economy/finance/windfall-tax-to-recoup-most-of-rs-1-lakh-cr-revenue-lost-in-excise-cuts/articleshow/92629748.cms

- https://www.business-standard.com/article/economy-policy/windfall-tax-to-generate-nearly-rs-94-800-cr-for-govt-says-moody-s-122070500464_1.html#:~:text=Photo%3A%20Shutterstock-,The%20windfall%20taxes%20on%20domestic%20crude%20oil%20production%20and%20fuel,Moody’s%20Investors%20Service%20said%20Tuesday.

- https://www.businessinsider.in/stock-market/news/gone-with-the-windfall-tax-ongc-loses-a-fifth-of-its-market-value/articleshow/92721451.cms

- https://www.dw.com/en/why-single-out-energy-companies-for-windfall-tax/a-62060966

- https://ongcindia.com/web/eng/about-ongc/performance

- https://www.ppac.gov.in/content/155_1_GasPrices.aspx

- https://tradingeconomics.com/commodity/natural-gas

- https://www.eia.gov/dnav/ng/ng_pri_fut_s1_d.htm

- https://economictimes.indiatimes.com/industry/energy/oil-gas/india-to-drop-windfall-tax-if-oil-prices-fall-40-a-barrel/articleshow/92646041.cms?from=mdr

- https://tradingeconomics.com/commodity/natural-gas

- https://www.eia.gov/dnav/ng/ng_pri_fut_s1_d.htm

- https://www.businesstoday.in/industry/energy/story/windfall-tax-to-shave-off-12-margin-for-ril-severely-hit-ongc-earnings-say-experts-340225-2022-07-04

- https://en.wikipedia.org/wiki/Windfall_tax

- https://www.moneycontrol.com/news/india/

- https://www.upstreamonline.com/opinion/india-s-windfall-tax-a-blow-for-oil-and-gas-sector/2-1-1252562

- https://en.wikipedia.org/wiki/Scandinavia

- https://mopng.gov.in/en

Click here to download full PDF.

📌Analysis of Bills and Acts

📌 Summary of Reports from Government Agencies

📌 Analysis of Election Manifestos